Understanding Collections & Bad Debt in Medical Billing

Collections and bad debt are where small front-end mistakes become expensive financial truths. A patient account does not become uncollectible overnight. It usually gets pushed there by weak eligibility checks, unclear financial communication, inaccurate patient responsibility, delayed statements, poor follow-up sequencing, unresolved insurance balances, or a billing team that treats collections as a last-stage task instead of a revenue cycle discipline. By the time the account reaches bad debt, the real failure often happened weeks earlier.

This guide explains collections and bad debt in medical billing the way revenue cycle teams actually need to understand them: as operational, financial, patient-experience, and compliance concepts that affect reimbursement, net collections, AR aging, write-offs, and trust. If your team wants fewer avoidable balances, cleaner patient responsibility, and stronger cash recovery without damaging patient relationships, these are the terms that matter.

1. Why collections and bad debt matter so much in medical billing

Collections in medical billing are not just about asking patients to pay. They are about correctly identifying patient liability, timing communication properly, preserving payer opportunities before shifting balances, and recovering revenue in a way that is legally defensible, operationally scalable, and financially rational. Teams that misunderstand collections terms often make the same costly mistakes repeatedly: they send statements before secondary insurance resolves, move balances to patient liability too early, ignore credit balances, apply inconsistent payment plan logic, or let small residual balances age until they harden into bad debt.

That matters because bad debt is rarely just a collections department problem. It is usually a revenue cycle visibility problem. The organization may be struggling with weak coordination of benefits, poor payment posting and management, unreliable patient responsibility and copay terms, or incomplete medical claims submission process controls long before collections staff ever touch the account.

Collections also matter because they sit at the intersection of patient communication and reimbursement integrity. When patients receive a bill for an amount that should still be under payer review, the organization does not just risk slower payment. It risks losing credibility. The patient starts to question every future bill, every EOB comparison, and every phone explanation. That is why strong collections performance depends on sharper command of Explanation of Benefits (EOB), claim adjustment reason codes CARCs, remittance advice remark codes RARCs, and overall revenue cycle management terms.

Then there is the financial reality. Every account that ages unnecessarily increases collection friction and decreases recovery probability. A balance that should have been resolved in the first statement cycle may become much harder to collect after multiple confusing statements, unreturned calls, payer miscues, and delayed follow-up. This is why organizations serious about reducing bad debt also watch revenue cycle KPIs, revenue leakage prevention, accurate medical billing and reimbursement, and denials prevention and management because patient collections are downstream from all of them.

Most importantly, bad debt is not just an accounting label. It is a lagging indicator of process breakdown. When bad debt rises, the correct question is not only “Why are patients not paying?” The better question is “What did the organization fail to clarify, collect, verify, or resolve before this balance reached the patient?” Teams that ask that question usually improve much faster than teams that only intensify outbound collections.

2. Core collections and bad debt terms every billing team should know

The first term to understand is patient responsibility. This is the portion of the account that the patient actually owes after benefit rules, payer adjudication, deductible status, copay structure, coinsurance logic, and any secondary insurance obligations are considered. It sounds basic, but this is one of the most mismanaged concepts in medical billing. If patient responsibility is overstated, the organization bills the patient unfairly. If it is understated, cash slows and balances reappear later in more confusing ways. That is why strong patient collections depend on accurate use of patient responsibility terms, commercial insurance billing terms, Medicare reimbursement terms, and coordination of benefits.

Next is self-pay. Many teams use this term too loosely. A true self-pay account is one where the patient is directly responsible because no billable insurance coverage applies to the service, the patient has no active coverage, or the balance has legitimately become patient liability after payer processing. What self-pay should not mean is “we are tired of waiting on insurance, so now it is on the patient.” That shortcut creates both operational and ethical risk. It is safer to distinguish true self-pay from unresolved insurance balances by using tighter controls in claims submission, clearinghouse terminology, practice management systems, and revenue cycle software terms.

Then comes bad debt itself. In medical billing, bad debt is generally the category used when a balance is judged uncollectible after defined internal collection efforts have been exhausted. But this definition becomes dangerous when organizations use bad debt as a catch-all for any stubborn balance. Bad debt should not absorb charity-eligible accounts, balances still tied to unresolved payer responsibility, claims affected by posting errors, or accounts that were never communicated properly in the first place. The cleaner your bad debt definition, the more useful your financial reporting becomes. This is why bad debt discussions belong alongside revenue cycle KPIs, revenue leakage insights, revenue cycle efficiency benchmarks, and impact of coding accuracy on hospital revenue.

Another essential term is charity care. Charity care is not failed collections. It is approved financial relief based on policy and eligibility. Teams that blur the line between charity care and bad debt corrupt both operational data and community trust. One reflects intentional patient support. The other reflects unrecovered collectible revenue. That distinction matters for workflow design, public reporting, and internal accountability.

Finally, every billing team should understand write-off in a much more disciplined way. A write-off is not one thing. It can be contractual, administrative, charity-based, or bad debt-related. When staff lump all write-offs together, they lose the ability to diagnose where revenue is actually failing. Collections teams need clean categories because improvement depends on knowing whether money disappeared due to payer contract rules, front-end process errors, patient hardship, or breakdown in follow-up discipline.

3. The real causes of bad debt in medical billing are usually upstream

Most organizations talk about bad debt too late. They discuss it when the account has already aged out, gone through statements, and maybe even landed in an agency queue. But by then, the real cause is usually upstream. The account may have started failing at eligibility, prior authorization, charge capture, payer sequencing, posting, or financial communication.

One major driver is unclear patient liability before and after service. If the patient does not understand what they may owe, when it becomes due, and why that amount might change after adjudication, collections become reactive and adversarial. This is why better bad debt performance often begins with cleaner SOAP notes and coding, stronger clinical documentation integrity, more accurate medical necessity criteria, and tighter essential guidelines for accurate clinical documentation. Documentation quality affects payer outcomes, and payer outcomes affect patient billing clarity.

Another driver is premature balance transfer. This happens when balances are moved to the patient before all insurance opportunities are exhausted or before the remit data has been fully interpreted. A team may see a remaining balance and assume it is collectible from the patient, even though a secondary payer should still be billed, a modifier-related underpayment should be appealed, or a posting defect distorted the remaining amount. That is why organizations with high patient complaints around billing usually need better command of claims reconciliation terms, coding edits and modifiers, CARCs, and RARCs.

A third driver is weak statement and outreach design. A balance can be legally valid and still be hard to collect because the communication strategy is poor. Vague statements, badly timed outreach, inconsistent portal messages, and no clear explanation of insurance activity all raise friction. Patients pay faster when the bill tells a credible story: what the service was, what insurance did, what remains, what payment options exist, and what to do if they believe something is wrong.

Then there is residual balance neglect. Small balances are often treated as harmless leftovers, but they are one of the fastest ways to accumulate preventable bad debt. Residual balances can come from coinsurance, posting mismatches, rounding, late corrections, secondary timing gaps, or micro-underpayments. If the organization sends repeated statements on balances that should have been investigated first, it wastes outreach capacity and degrades patient trust at scale.

4. Collections workflow terms that determine whether balances get paid or go bad

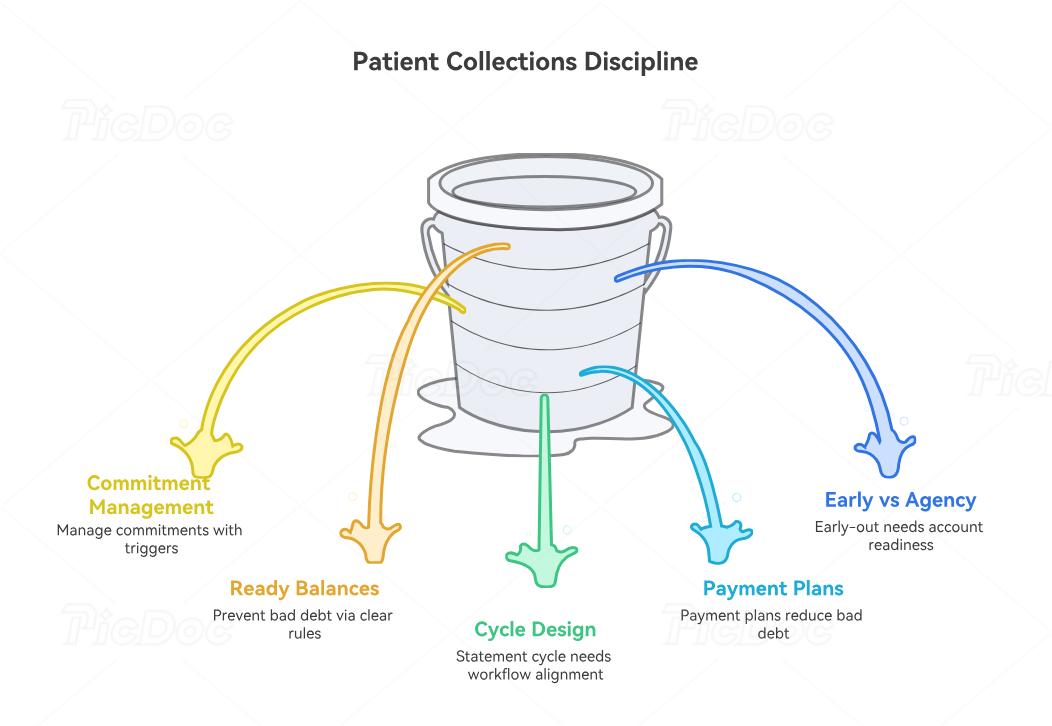

A strong patient collections process is built on workflow discipline, not random follow-up. That is why terms like statement cycle, payment plan, partial payment, promise to pay, early-out, and agency placement matter so much. They define how the organization behaves once a patient balance becomes real.

The statement cycle is the cadence through which patients are notified about their balances. This is not just a mailing schedule. It is a strategy lever. If the first statement is delayed too long after payer adjudication, urgency drops and account recall weakens. If it is sent too early, while insurance questions still exist, confusion rises. Good statement-cycle design depends on clean handoffs from payment posting, accurate medical billing software workflows, better EHR integration terms, and sharper RCM software rules.

A payment plan is more than a convenience feature. It is a collections conversion tool for balances that are valid but difficult to satisfy in one payment. Without clear payment-plan rules, staff improvise, patients receive inconsistent treatment, and follow-up becomes messy. Effective payment-plan design accounts for balance size, prior payment behavior, patient hardship indicators, and the cost of future follow-up. When it is done well, it reduces bad debt without requiring aggressive agency escalation.

Partial payment and promise to pay are two terms that sound helpful but often fail operationally because teams do not manage them like commitments. A partial payment should change the next follow-up path intentionally. A promise to pay should be recorded with amount, date, and consequence of nonpayment. If these are just call-center notes with no workflow trigger, they create the illusion of progress while balances continue aging.

Then there is early-out versus collection agency placement. Early-out programs usually aim to engage patients before the account is formally treated as bad debt, often using softer communication and more payment-option flexibility. Agency placement is a later-stage recovery method that may improve some recoveries but can also introduce patient-experience and brand risk if account quality is poor. The key issue is account readiness. If unresolved insurance balances, credit balances, or charity-screening opportunities still exist, outside placement is not collections discipline. It is process abandonment.

That is why the smartest teams define patient-ready balances explicitly. They decide what must be true before an account is allowed into patient collections: insurance fully adjudicated, no unresolved COB, no credit conflict, no active appeal, no pending correction, and no obvious charity-screening gap. That one concept alone can prevent a huge amount of avoidable bad debt and patient mistrust.

5. How to reduce bad debt without turning patient collections into chaos

Reducing bad debt is not about becoming more aggressive first. It is about becoming more accurate first. An organization that bills the right balance, at the right time, with the right explanation, will almost always outperform one that simply adds more collection touches to a messy process.

The first move is to tighten patient-balance integrity. Before a balance enters the statement workflow, ask whether the account has cleared the key financial gates. Has the primary payer fully adjudicated? Has the secondary been billed or ruled out correctly? Have the claim adjustment reason codes been interpreted correctly? Has payment posting preserved the real patient liability rather than defaulting unresolved amounts into self-pay? Has the account been checked against medical billing reconciliation logic and revenue leakage prevention?

The second move is to treat bad debt as a segmented outcome, not a single bucket. Separate accounts that failed because of patient hardship, balances that failed because of poor communication, and balances that failed because the organization shifted liability incorrectly. Once these categories are visible, improvement becomes much more precise. You can redesign front-end counseling, tune statement strategy, or repair posting rules rather than blindly tightening agency placements.

The third move is to improve front-end and pre-service collections discipline. Point-of-service collections are not about squeezing patients. They are about reducing avoidable downstream confusion when the likely patient portion is already known. This works best when estimates are presented honestly, payment options are clear, and staff know the difference between an estimate and a final adjudicated amount.

The fourth move is to protect small-balance logic. Residual balances need more scrutiny, not less. Many tiny balances are created by preventable defects: unapplied payments, late payer adjustments, duplicate statement timing, or secondary errors. Sending repeated bills on those balances does not prove operational strength. It proves the organization cannot distinguish collectible debt from workflow residue.

Finally, measure what matters. Track bad debt by source, not just total dollars. Track how many patient statements went out on balances that were later corrected. Track how many agency placements were pulled back because insurance was still active. Track credit balances that were present at the moment a statement was generated. Track the share of bad debt that could have been prevented earlier in the revenue cycle. Those are the metrics that actually change behavior.

6. FAQs about collections and bad debt in medical billing

-

Patient collections refers to the process of recovering valid patient balances through statements, calls, portals, payment plans, and other follow-up methods. Bad debt is the category used when those balances are ultimately judged uncollectible after defined collection efforts. Collections is the process. Bad debt is one possible outcome of failed recovery.

-

No. Many unpaid balances are still in active collections, still awaiting insurance resolution, still eligible for charity review, or still affected by posting or COB issues. Calling them bad debt too early hides the real cause of nonpayment and distorts performance reporting.

-

Some of the most preventable causes are premature patient billing, inaccurate patient responsibility, unresolved secondary insurance, poor statement timing, weak payment-plan workflows, and failure to screen for financial assistance early enough. Upstream process errors create a large share of downstream bad debt.

-

Charity care reflects approved financial assistance based on policy and eligibility. Bad debt reflects balances that were considered collectible but were not recovered after collections efforts. The two should never be blended because they represent different realities, different policies, and different operational fixes.

-

Because they are often sent automatically without enough investigation. Small balances may come from posting defects, COB timing issues, minor payer adjustments, or residual workflow errors. When organizations treat every residual balance as immediately collectible, they flood patients with low-trust bills and quietly build avoidable bad debt.

-

Start by improving balance accuracy before statement generation. Make sure insurance is fully resolved, patient responsibility is validated, credits are reviewed, and charity-screening opportunities are identified early. Then strengthen statement timing, payment-plan design, and follow-up consistency. Reducing bad debt usually starts with cleaner revenue cycle control, not harder collections language.